How To Figure Out Dti

What Is Debt To Income Ratio Info Glue

infoglue.org

What Is The Debt To Income Dti Ratio How To Calculate It Personal Loan Blogs By Finserv Markets

www.bajajfinservmarkets.in

How To Calculate Your Debt To Income Ratio Step By Step Mymove

www.mymove.com

How To Calculate Dti Debt To Income Ratio Broke Millennial Author Erin Lowry

www.yahoo.com

Frontend Backend Debt To Income Calculator Dti Mortgage Qualification Calculator

www.carpaymentcalculator.net

What Is Dti Debt To Income Ratio Explained Residential Mortgage Services Blog

rmsmortgage.com

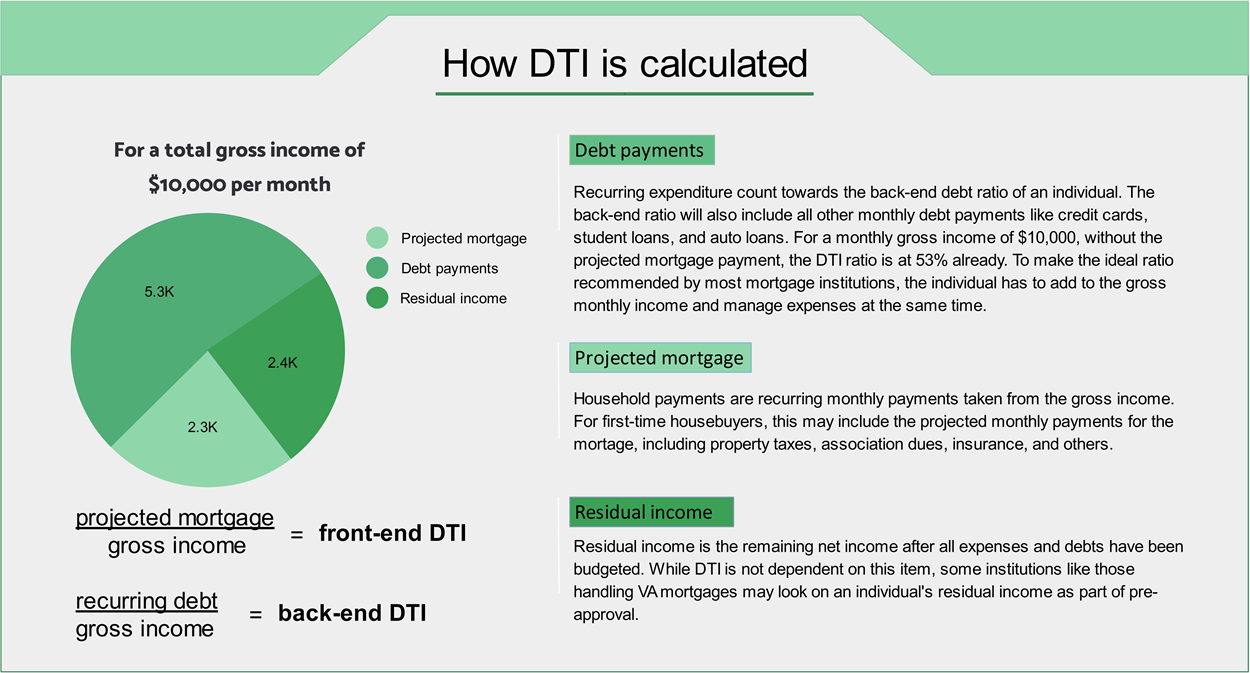

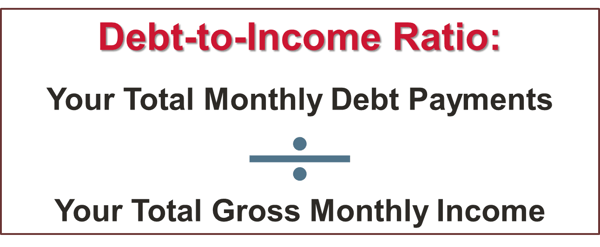

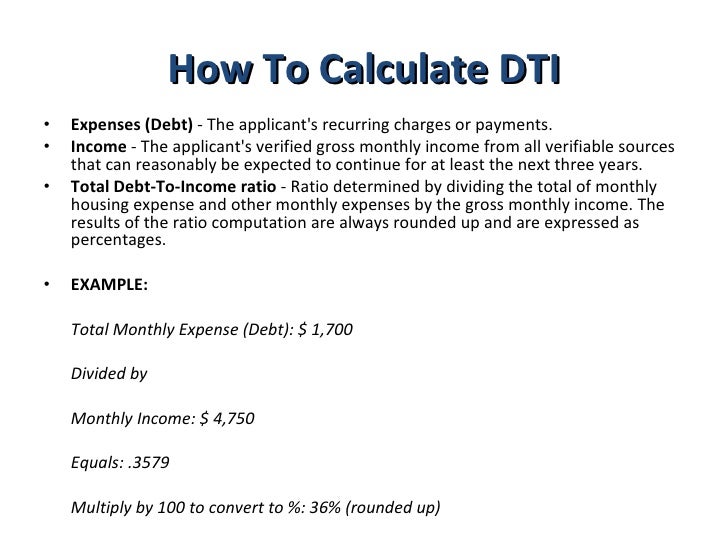

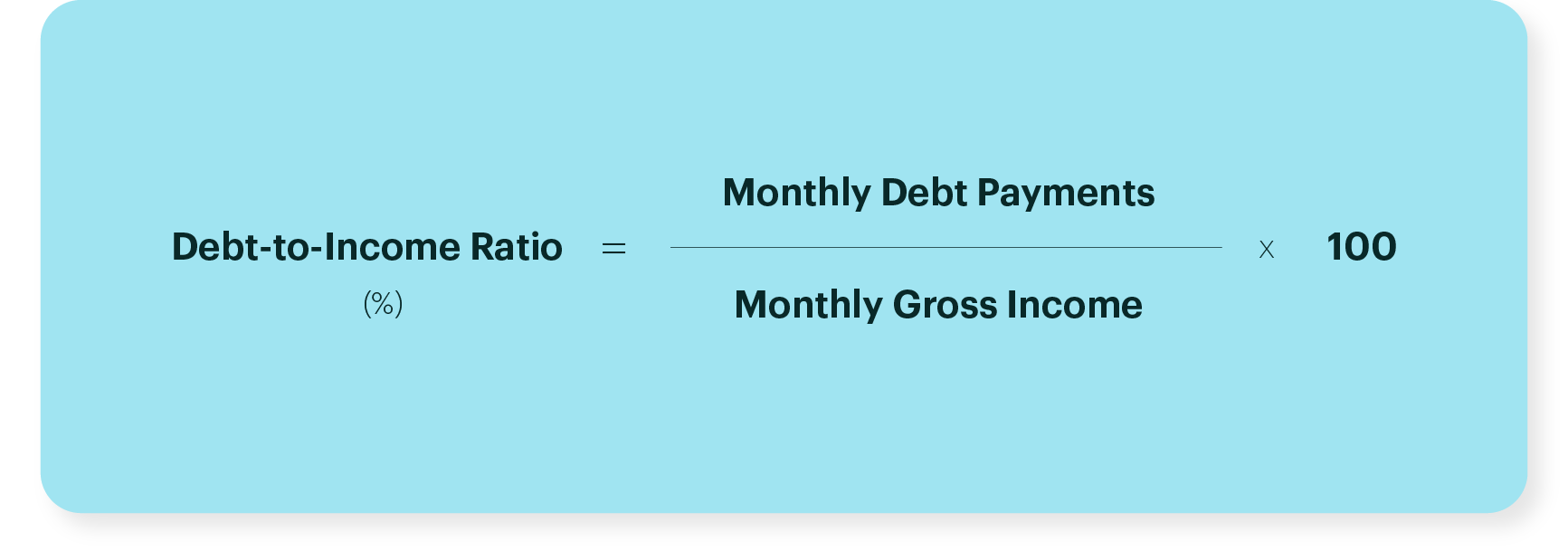

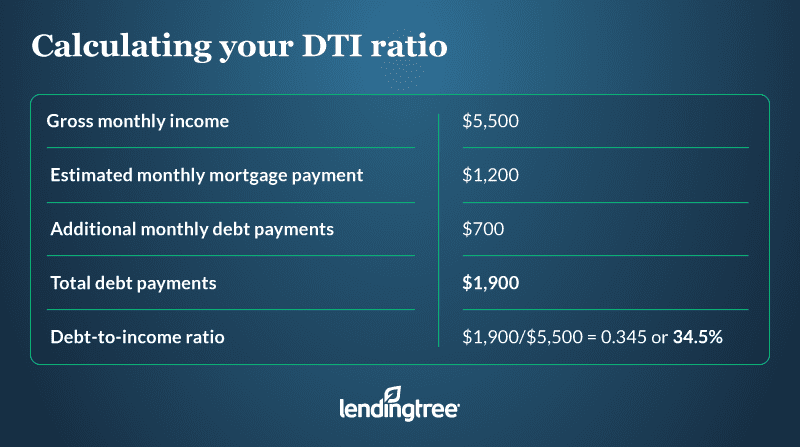

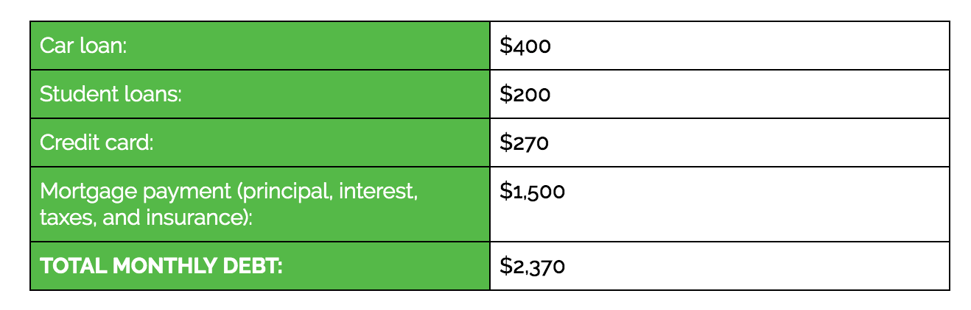

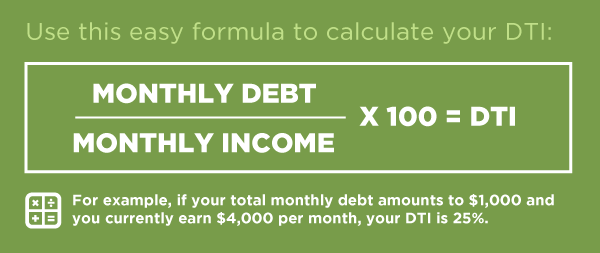

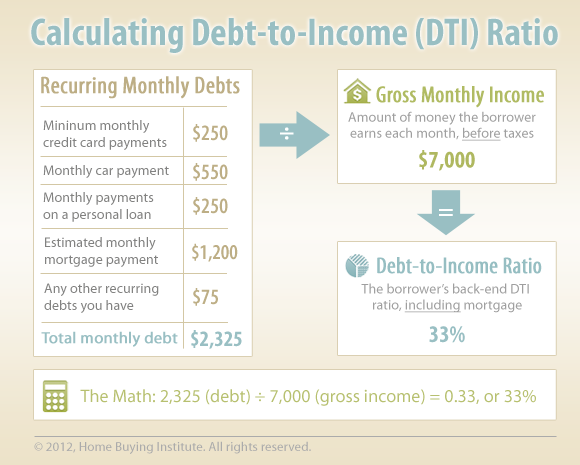

For instance if your debt costs 2000 per month and your monthly income equals 6000 your dti is 2000 6000 or 33 percent.

How to figure out dti. You can calculate your dti by adding up your monthly minimum debt payments and dividing it by your monthly pre tax income. Well help you understand what it means for you. The dti ratio you need for loan approval when you apply for a mortgage or any other type of loan the lender calculates your future debt to income ratio.

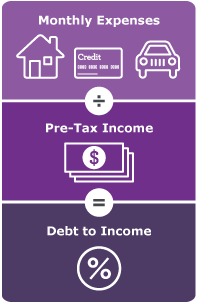

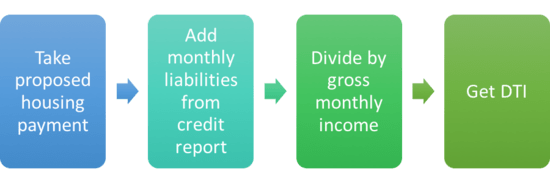

Then adjust the gross monthly. A debt to income or dti ratio is derived by dividing your monthly debt payments by your monthly gross income. The front end dti is typically calculated as housing.

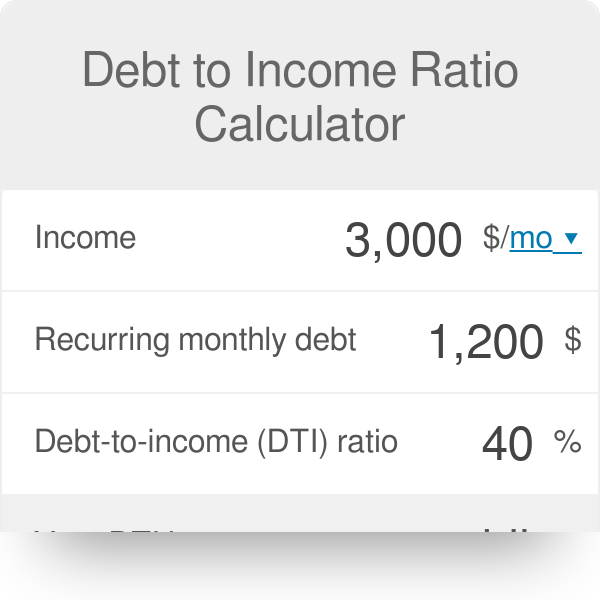

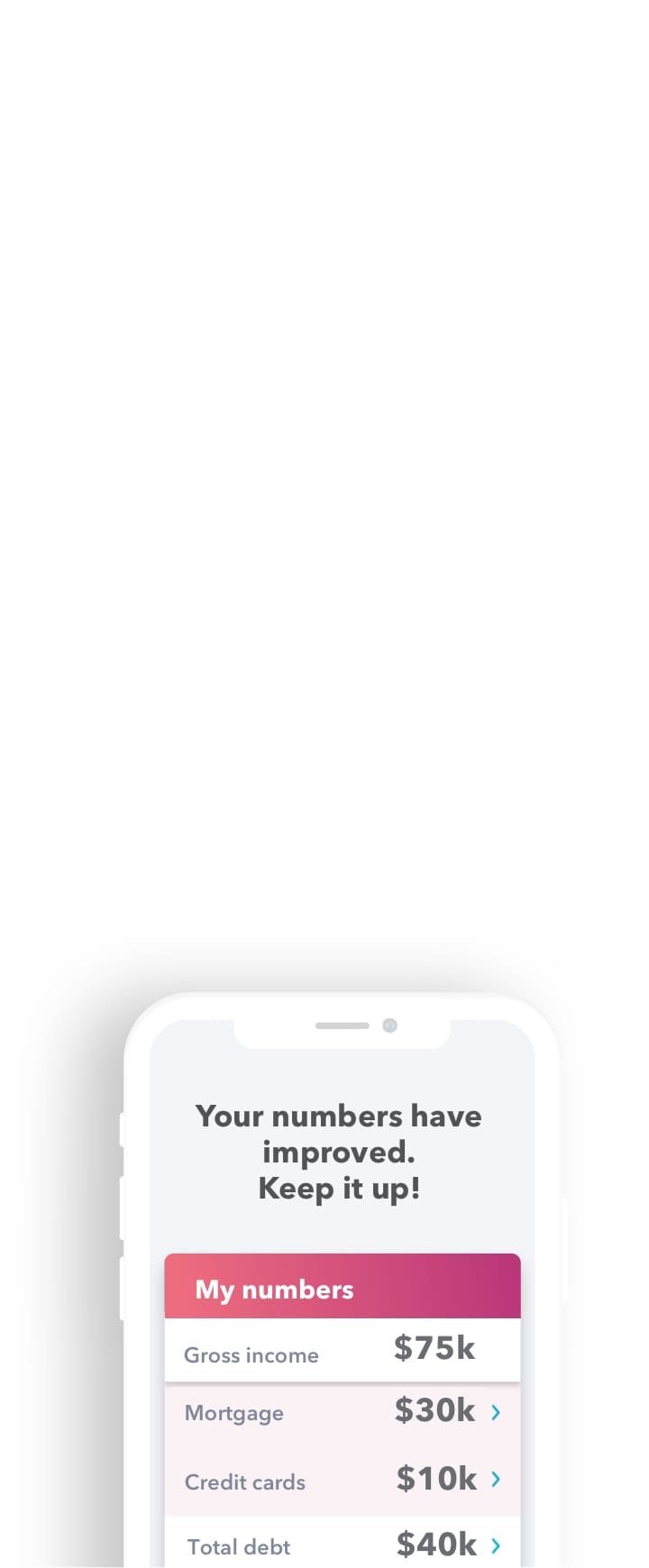

To calculate your dti enter the payments you owe such as rent or mortgage student loan and auto loan payments credit card minimums and other regular payments. If they had no debt their ratio is 0. The result is your dti which will be in the form of a percentage.

Dti monthly debt monthly income the first step in calculating your debt to income ratio is determining how much you spend each month on debt. To calculate your estimated dti ratio simply enter your current income and payments. Keep in mind that the underwriter assesses your future debt ratio not the one you have right now.

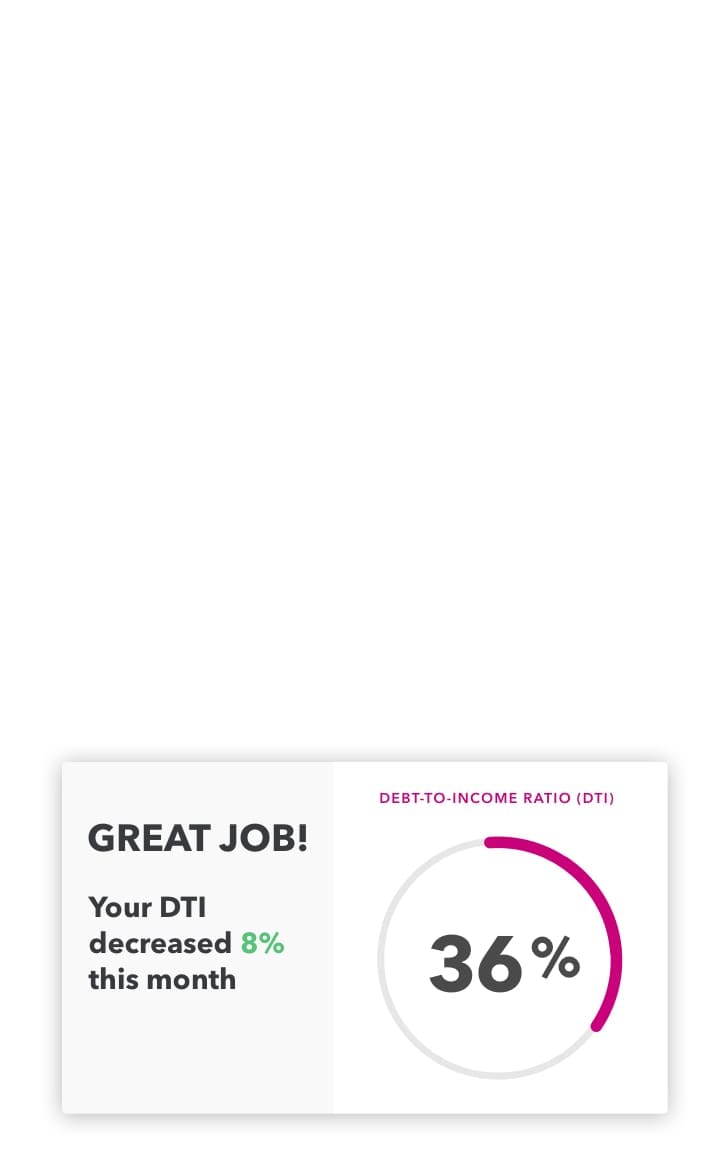

The sweet spot for approval is a ratio of 41 or less. The lower the dti. Divide the total by your gross monthly income which is your income before taxes.

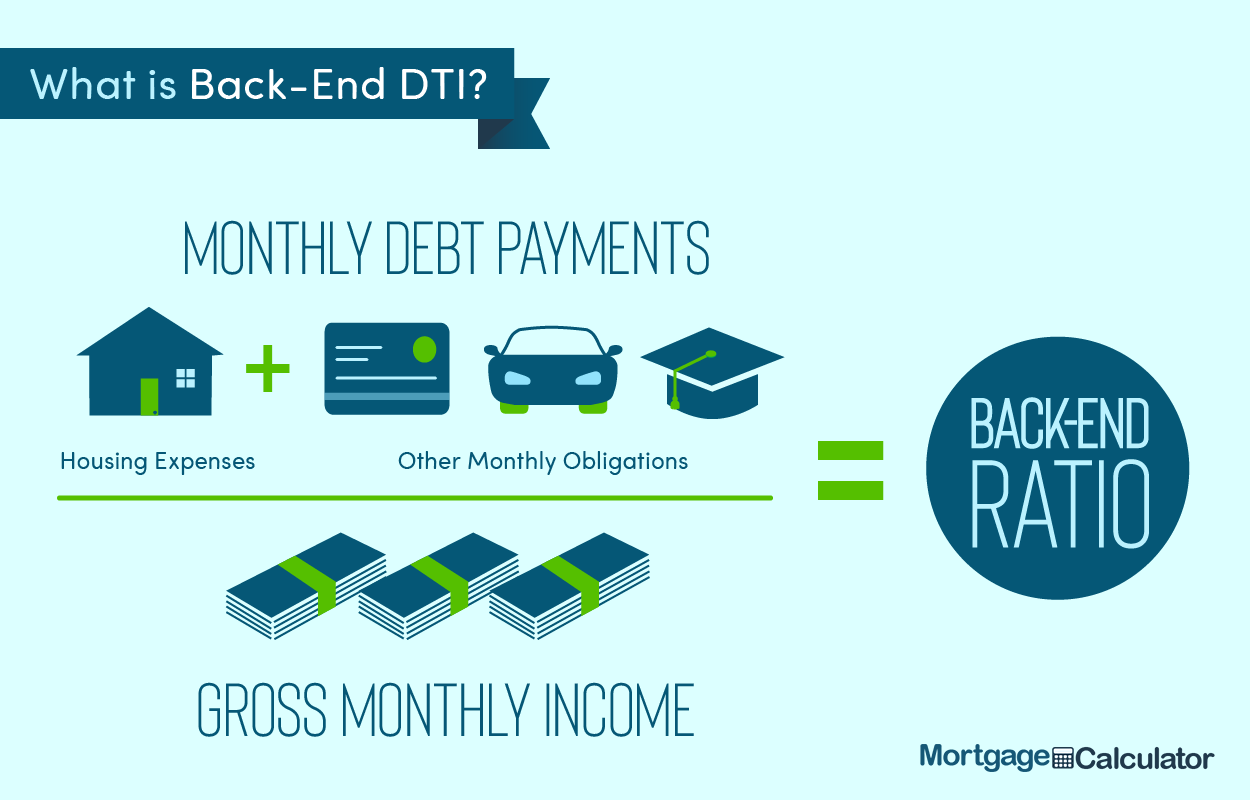

The less risky you are to lenders. The front end debt to income ratio dti or the housing ratio calculates how much of a persons gross income is spent on housing costs. The ratio is expressed as a percentage and lenders use it to determine how well you.

As a quick example if someones monthly income is 1000 and they spend 480 on debt each month their dti ratio is 48. To determine your dti ratio simply take your total debt figure and divide it by your income. Debt to income ratio dti is the ratio of total debt payments divided by gross income before tax expressed as a percentage usually on either a monthly or annual basis.

What Is Debt To Income Ratio And Why Does It Matter Experian

www.experian.com

Debt To Income Ratio How To Calculate Your Dti Nerdwallet

www.nerdwallet.com

Debt To Income Ratio Calculator For Mortgage Approval Dti Calculator

www.mortgagecalculator.org

What Is Debt To Income Ratio And Why Does It Matter Credit Karma

www.creditkarma.com

What S A Good Debt To Income Ratio Dti Debt Relief Debt To Income Ratio Freedom Debt Relief

www.pinterest.com

Debt To Income Ratio Calculator

www.omnicalculator.com

Debt To Income Ratio Calculating Understanding Dti Intuit Turbo

turbo.intuit.com

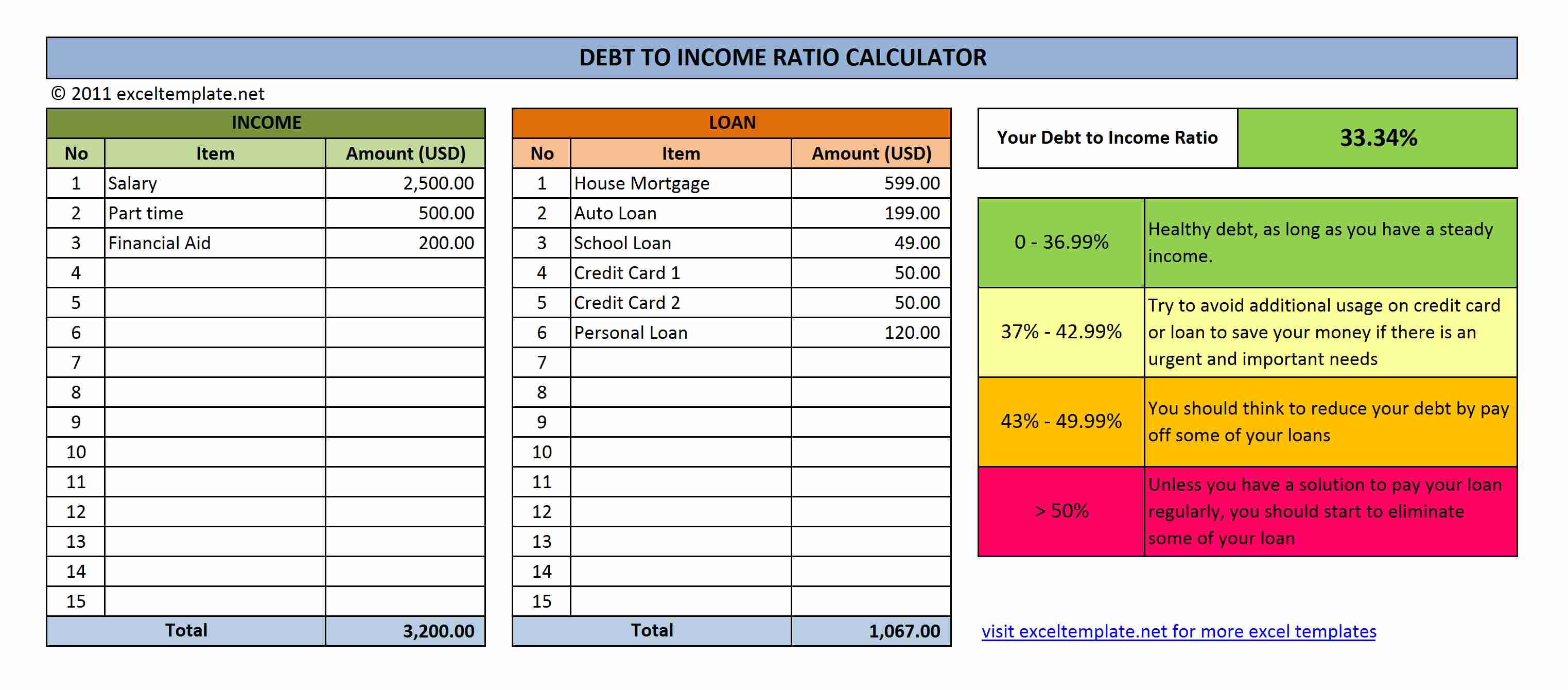

Debt To Income Dti Ratio Calculator Excel Templates

exceltemplates.net

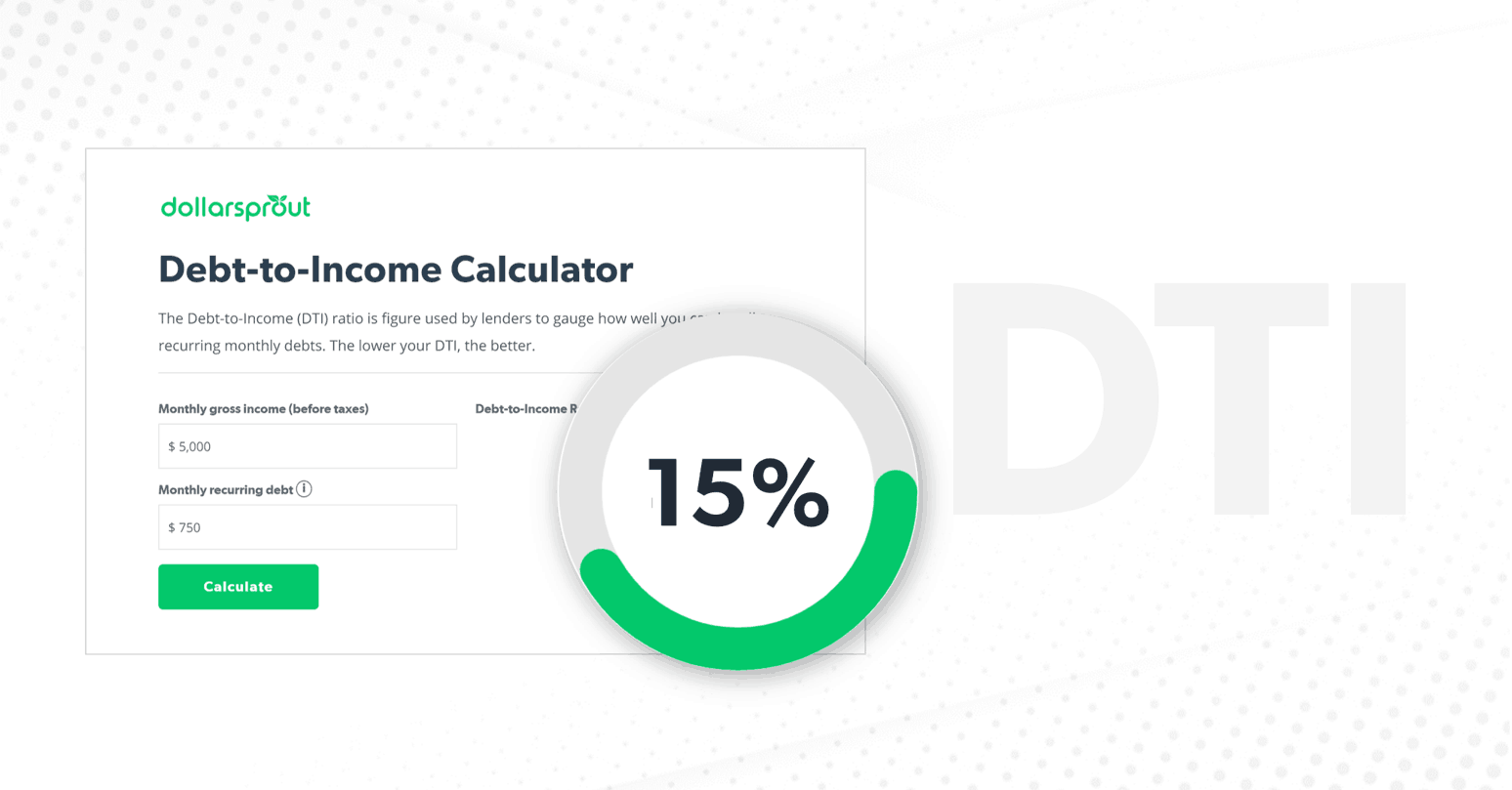

Debt To Income Calculator Dollarsprout

dollarsprout.com

Debt To Income Ratio What It Is And How To Improve Yours Student Loan Hero

studentloanhero.com

Debt To Income Ratio Calculator For Mortgage Approval Dti Calculator

www.mortgagecalculator.org

Debt To Income Ratio Calculator For Mortgage Approval Dti Calculator

www.mortgagecalculator.org

Know How To Calculate Your Debt To Income Ratio

www.sunshinestatemortgage.net

Debt To Income Ratio Meaning Formula How To Calculate Dti

www.wallstreetmojo.com

How To Manage Your Debt And Improve Your Dti Ratio

blog.lmcu.org

Debt To Income Ratio How To Calculate Improve It Lendingclub

www.lendingclub.com

Calculate Your Debt To Income Ratio Wells Fargo

www.wellsfargo.com

Dti Or Debt To Income Ratio Explained The Money Coach

askthemoneycoach.com

Do You Know Your Debt To Income Ratio Dti Here S How To Figure It Out

avocadoughtoast.com

/GettyImages-463012867-572e2cbb5f9b58c34c8fa655.jpg)

What S Considered A Good Debt To Income Dti Ratio

www.investopedia.com

What You Should Know About Debt To Income Ratios

www.firstalliancecu.com

Https Www Corelogic Com Blog 2020 8 Conventional Loans Near 60 Of The 1 8 Million Loans With A Dti Over 43 Percent Aspx

www.corelogic.com

Debt To Income Ratio Calculating Understanding Dti Intuit Turbo

turbo.intuit.com

Debt To Income Ratio Dti What It Is And How To Calculate It The Truth About Mortgage Com

www.thetruthaboutmortgage.com

Debt To Income Ratio How To Calculate Your Dti Nerdwallet

www.nerdwallet.com

A Guide To Debt To Income Ratio Dti Rocket Mortgage

www.rocketmortgage.com

Debt To Income Ratio How To Calculate Your Dti

www.quickenloans.com

Debt To Income Ratio Calculator For Mortgage Approval Dti Calculator

www.mortgagecalculator.org

Understanding Debt To Income Dti

www.slideshare.net

How To Calculate Your Debt To Income Ratio Dti Credit Knocks Build And Repair Credit Save Money On Loans

www.creditknocks.com

Fha Debt To Income Dti Ratio Requirements 2019

www.fhahandbook.com

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsw Gtjzb Tx01rrbcjy8hdeplu79d9fta Nlorvk37 Tacrw3w Usqp Cau

encrypted-tbn0.gstatic.com

Calculating Business Debt To Income Ratio Fast Capital 360

www.fastcapital360.com

How To Lower Your Debt To Income Ratio Dti For A Mortgage Better Mortgage

better.com

Debt To Income Ratio Calculator For Mortgage Approval Dti Calculator

www.mortgagecalculator.org

What You Should Know About Debt To Income Ratios

www.firstalliancecu.com

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctgmhidslbdz Pjfaea 9ptke8jgud4c8k8snhnkarth82vjfnc Usqp Cau

encrypted-tbn0.gstatic.com

Debt To Income Ratio Calculating Understanding Dti Intuit Turbo

turbo.intuit.com

Debt To Income Ratio How To Calculate Improve It Lendingclub

www.lendingclub.com

Dti Requirements For Usda Loans

www.usdaloans.com

/DTIjpeg-5c5253f846e0fb000167ce85.jpg)

Qualifying Ratios Definition

www.investopedia.com

How To Calculate Your Debt To Income Ratio Lendingtree

www.lendingtree.com

Debt To Income Ratio How To Calculate Dti Formula

fitsmallbusiness.com

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsipkbo2mxjz3wc3lofk5mtncxchs2ugaywm8z7s65 Raf2ukpv Usqp Cau

encrypted-tbn0.gstatic.com

Https Www Corelogic Com Blog 2020 8 Conventional Loans Near 60 Of The 1 8 Million Loans With A Dti Over 43 Percent Aspx

www.corelogic.com

Debt To Income Ratio Learn Calculate And Improve

www.bills.com

Debt To Income Dti Ratio Guidelines For Va Loans

www.veteransunited.com

How To Calculate Improve Your Debt To Income Dti Ratio

www.merchantmaverick.com

Debt To Income Dti Credit Com

www.credit.com

Loan Status With Dti Download Scientific Diagram

www.researchgate.net

Https Www Corelogic Com Blog 2020 8 Conventional Loans Near 60 Of The 1 8 Million Loans With A Dti Over 43 Percent Aspx

www.corelogic.com

What Is Debt To Income Ratio How Do I Calculate My Dti

www.fedhomeloan.org

How To Calculate Improve Your Debt To Income Dti Ratio

www.merchantmaverick.com

How Debt Burden Affects Fha Mortgage Repayment In Six Charts Urban Institute

www.urban.org

How To Calculate Your Debt To Income Ratio Dti Credit Knocks Build And Repair Credit Save Money On Loans

www.creditknocks.com

Debt To Income Ratio How To Calculate Your Dti

www.quickenloans.com

Why Dti Is Important Selling North Texas Homes

www.yourtexasdream.com

How Debt To Income Ratio Affects Mortgages

bettermoneyhabits.bankofamerica.com

Calculating Debt To Income Ratio What Does The Dti Ratio Tell You

consumerdebtadvice.ca

Debt To Income Dti Ratio Definition

www.investopedia.com

How Self Employed Workers Get Mortgages

www.newcastle.loans

How To Calculate Your Debt To Income Ratio And What It Means Intuit Turbo Blog

turbo.intuit.com

How To Calculate Debt To Income Ratio Dti What It Means Badcredit Org

www.badcredit.org

How To Calculate Your Debt To Income Ratio Dti Credit Knocks Build And Repair Credit Save Money On Loans

www.creditknocks.com

How To Lower Your Debt To Income Ratio Dti For A Mortgage Better Mortgage

better.com

Https Www Corelogic Com Blog 2020 8 Conventional Loans Near 60 Of The 1 8 Million Loans With A Dti Over 43 Percent Aspx

www.corelogic.com

1

encrypted-tbn0.gstatic.com

How To Calculate Debt To Income Dti Ratios Youtube

www.youtube.com

Debt To Income Ratio Calculator Zillow

www.zillow.com

How To Calculate Debt To Income Dti Ratios Youtube

www.youtube.com

Dti Went Well Now I Need To Figure Out How To Look At It Broken Brain Brilliant Mind

brokenbrilliant.wordpress.com

What Is A Good Debt To Income Ratio For A Mortgage Intuit Turbo Blog

turbo.intuit.com

/debt-ratio-on-blackboard-with-hand-172449346-5b01bd2118ba0100376172ce.jpg)

How To Calculate Your Debt To Income Ratio

www.thebalance.com

Debt To Income Ratio

moneyfit.org

Https Www Corelogic Com Blog 2020 8 Conventional Loans Near 60 Of The 1 8 Million Loans With A Dti Over 43 Percent Aspx

www.corelogic.com

Debt To Income Ratios How To Calculate And Interpret Your Dti Plus What To Do If Yours Is Bad

www.thedebthustler.com

Debt To Income Ratio Meaning Formula How To Calculate Dti

www.wallstreetmojo.com

How To Calculate Debt To Income Ratio Dti Ratio

www.moolanomy.com

What Debt To Income Ratio Is Good When Applying For A Mortgage

www.cutx.org

4 Budgeting Ideas To Figure Out How Much Home You Can Afford

latest.laketrust.org

How To Calculate Your Debt To Income Ratio And What It Means Intuit Turbo Blog

turbo.intuit.com

Schematic Description Of The Main Dti Parameters Download Table

www.researchgate.net

Calculate Your Debt To Income Ratio Wells Fargo

www.wellsfargo.com

How To Lower Your Debt To Income Ratio

www.onemainfinancial.com

How Debt Burden Affects Fha Mortgage Repayment In Six Charts Urban Institute

www.urban.org

Debt To Income Ratio Calculator Zillow

www.zillow.com

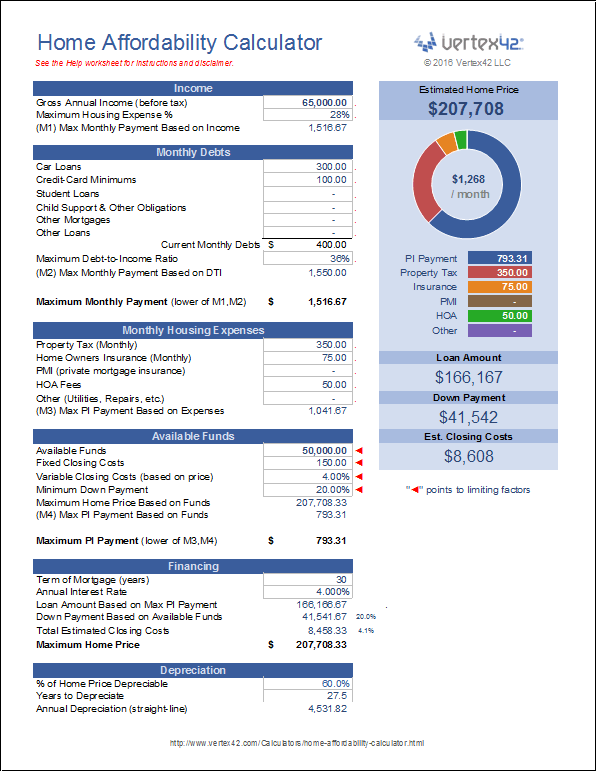

Home Affordability Calculator For Excel

www.vertex42.com

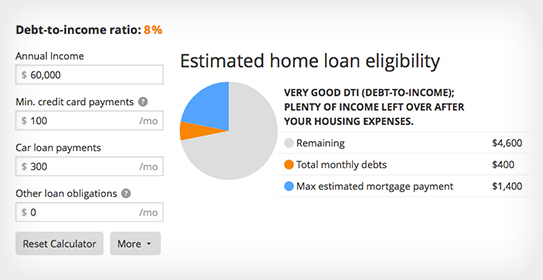

How Much House Can I Afford Debt To Income Calculator The Loaded Pig

www.theloadedpig.com

Debt To Income Ratio Dti Calculator

www.calculatestuff.com

Debt To Income Dti Calculator Interest Co Nz

www.interest.co.nz

What Is Dti Ratio How To Calculate Debt To Income Easily

perfectionhangover.com

Dti And Network Construction Based On The Automated Anatomical Download Scientific Diagram

www.researchgate.net

What Is Dti Ratio How To Calculate Debt To Income Easily Debt Debt To Income Ratio Mortgage Loans

www.pinterest.com

Debt To Income Ratio Dti Limits For 2014 Fha Conventional And Qm

www.homebuyinginstitute.com

Mortgage Related Dti By Income Level Notes The Figure Shows The Download Scientific Diagram

www.researchgate.net

How Much Debt Is Too Much Citizens Bank

www.citizensbank.com

What S A Deb To Income Ratio And Does It Matter

www.greenwoodhomesrealty.com

Dti Debt To Income Ratio Definition And Data

www.bills.com